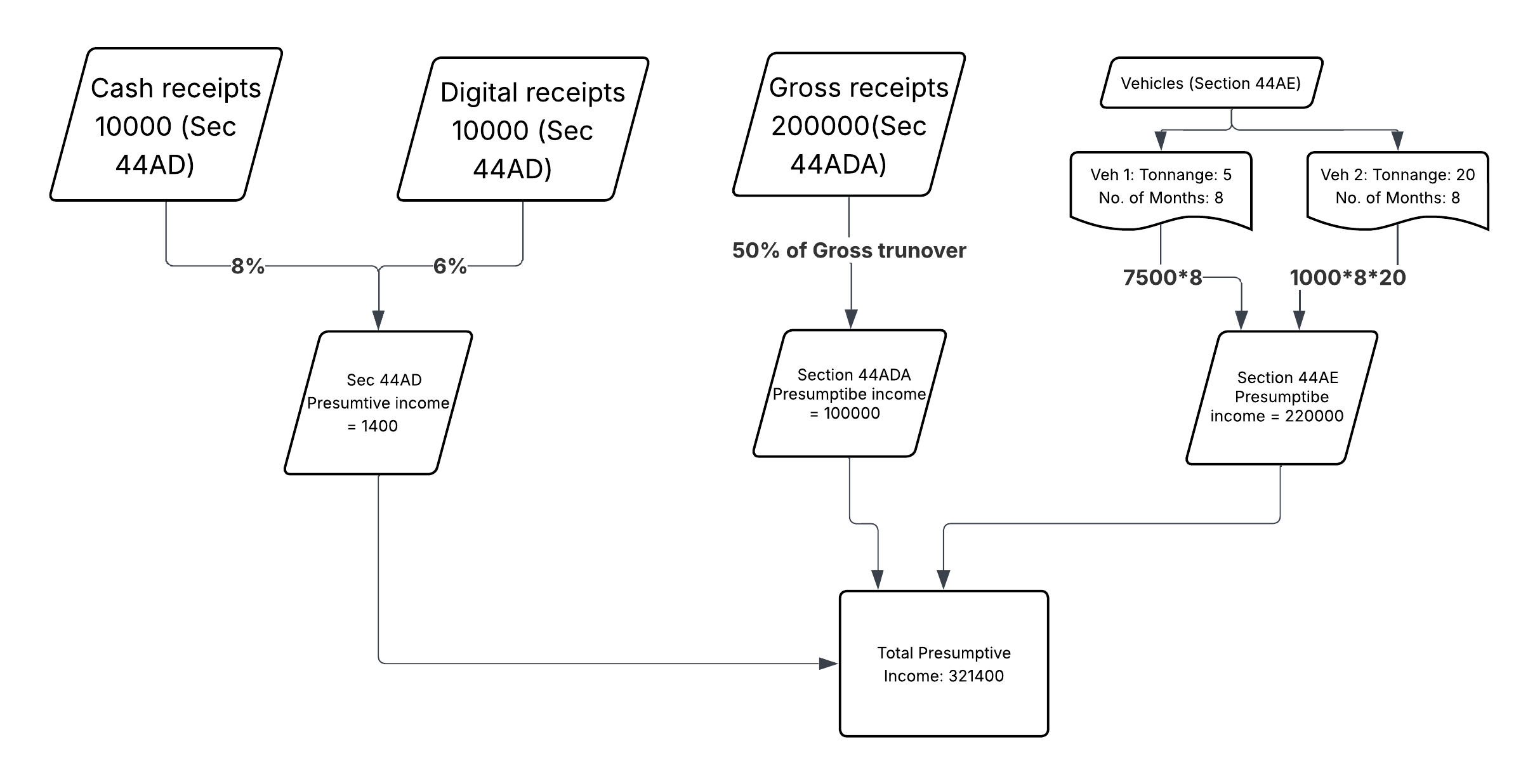

The Presumptive Taxation Scheme (PTS) under the Income Tax Act, 1961 is designed to simplify tax compliance for small businesses, professionals, and transport operators. Instead of maintaining detailed books of account and undergoing tax audits, eligible taxpayers can declare income at a fixed, pre determined percentage of their turnover or receipts. This reduces compliance burden, ensures predictability, and encourages voluntary tax compliance. PTS is primarily governed by Sections 44AD, 44ADA, and 44AE. The following figure illustrates the calculation for presumptive income under various sections.

The net taxable income under section 44AE will be determined as follows: Rs 1000 per ton of gross vehicle weight for heavy goods vehicles (these have a gross vehicle weight exceeding 12 tons) per month. For a lightweight vehicle (tonnage less than or equal to 12), the rate is Rs 7500 per month. Net income under section 44 AE is the sum of income from all the vehicles.

Purpose of Presumptive Taxation

Presumptive taxation is built on a simple idea: When taxpayers are small and compliance costs are high, the law “presumes” a reasonable level of income instead of requiring detailed accounting. This approach aims to:

- Reduce compliance burden and cost for small taxpayers

- Provide certainty in income computation

- Encourage more people to come under the tax net

- Avoid the need for maintaining books and getting audits done (in most cases)

Section 44AD — For Small Businesses

Eligibility

- Resident Individuals, HUFs, and Partnership Firms (excluding LLPs)

- Engaged in any business except:

- Agency business

- Commission or brokerage

- Goods carriage business (covered under 44AE)

- Professions listed under Section 44AA(1)

Turnover Limit

- Standard limit: ₹2 crore

- Enhanced limit: ₹3 crore, if cash receipts are less than or equal to 5% of total turnover

Presumptive Income

- 8% of turnover (for cash receipts)

- 6% of turnover (for digital receipts)

Key Features

- No need to maintain books under Section 44AA

- No audit under Section 44AB

- No further expense deductions allowed (income is final)

- Once opted, must continue for 5 years; discontinuation triggers a 5 year lockout from the scheme

Section 44ADA — For Specified Professionals

Eligible Professions

- Legal

- Medical

- Engineering

- Architecture

- Accountancy

- Technical consultancy

- Interior decoration

- Other notified professions

Eligible Assessees

- Resident Individuals and Partnership Firms (excluding LLPs)

Gross Receipts Limit

- Up to ₹50 lakh (enhanced to ₹75 lakh if cash receipts less than or equal to 5%)

Presumptive Income

- 50% of gross receipts is deemed as income

Key Features

- No need to maintain books

- No audit required unless:

- Income declared is less than 50%, and

- Total income exceeds the basic exemption limit

Section 44AE — For Goods Carriage Businesses

Eligibility

- Any person owning not more than 10 goods carriages at any time during the year

Presumptive Income

- For heavy vehicles: ₹1,000 per ton per month

- For other vehicles: ₹7,500 per month per vehicle

Key Features

- No need to maintain books

- Income is deemed and final

- Applies irrespective of actual profit or loss

Common Benefits Across All Presumptive Schemes

- No books of account required under Section 44AA

- No tax audit under Section 44AB (unless declaring lower income)

- Simplified compliance and reduced professional costs

- Advance tax: only one installment by 15th March is required

Limitations and Cautions

- Not available to companies or LLPs (except 44AE for any person)

- Not available if deductions under Sections 10A, 10AA, 10B, 10BA, or Chapter VI A (certain incomes) are claimed

- Once 44AD is opted and then exited, a 5 year lockout applies

- Presumptive income is final — no further expense claims allowed

- Professionals under 44ADA cannot claim depreciation separately (it is deemed included)

General Notes And Disclaimer

- While our presumptive income tax calculator is designed to be user-friendly and helpful for your convenience, it is not a substitute for professional advice. Taxpayers are encouraged to consult a qualified Chartered Accountant (CA) for personalized guidance regarding their tax filings. Additionally, please refer to the official website or the e-filing portal of the Income Tax Department for the most accurate and up-to-date information. Please navigate to this page to know more.

- This tax calculation assumes that you do not have any salary income.

- Under section 44AD, the presumptive income is deemed to be 8% of turnover for cash receipts and 6% for digital receipts. For section 44ADA, it is considered as 50% of gross receipts.

- This calculator accommodates both the presumptive portion of income and the total business

income.

You

may alternate between these options at any time. It should be noted that the presumptive

portion of

your

business income is typically lower than your total business income

due

to

the application of these reduced presumptive rates.

- 8% of for cash receipts + 6% for digital receipts under section 44AD

- + 50% of gross receipts under section 44ADA

- + Income calculated as per section 44AE provisions (elaborated below)

- The net taxable income under section 44AE will be determined as follows: Rs 1000 per ton of gross vehicle weight for heavy goods vehicles (these have a gross vehicle weight exceeding 12 tons) per month. For a lightweight vehicle (tonnage less than or equal to 12), the rate is Rs 7500 per month. Net income under section 44 AE is the sum of income from all the vehicles.

- In accordance with Section 44AE, any part of a month in which the goods carriage was owned shall be treated as a full month for the purpose of income calculation.

- Please ensure you utilise this calculator to determine your tax liability, confirm the accuracy of the calculation with your tax advisor, and remit the advance tax accordingly. Under the presumptive taxation scheme, the deadline for advance tax payment is 15th March of the financial year.